Unjustified price increases, erosion of quality, growing inequalities, and an identity crisis: the global luxury sector is undergoing its deepest reckoning since the Great Recession of 2008. At the Financial Times’ “Business of Luxury Summit” in Barcelona, major maisons were confronted with an unvarnished reality: they have lost 50 million customers in just two years.

Unjustified price increases, erosion of quality, growing inequalities, and an identity crisis: the global luxury sector is undergoing its deepest reckoning since the Great Recession of 2008. At the Financial Times’ “Business of Luxury Summit” in Barcelona, major maisons were confronted with an unvarnished reality: they have lost 50 million customers in just two years.

A downturn unseen since 2008

Until a few years ago, luxury seemed immune to crises. After the shock of the pandemic, the sector experienced a sharp rebound, driven by a desire for compensation and a wealthy clientele whose savings had swelled during lockdowns. Fashion houses were breaking record after record. Louis Vuitton, Chanel, Hermès: their queues themselves became a status symbol.

But the euphoria was short-lived. 2024 marked the most difficult year for the industry in fifteen years, excluding the Covid period. Global luxury spending fell by around €1.5 trillion, down 2% compared to 2023. And forecasts for 2025 are even darker: the most likely scenario points to a decline in personal luxury goods sales between 2% and 5%, an unprecedented trend since the 2008 global financial crisis.

The “Very Important Customers” (VIC) segment, representing only 2% of the clientele, generates nearly 40% of total sector revenue. The loss of aspirational customers structurally weakens the model.

What stands out beyond the figures is the human scale of the collapse: 50 million consumers have turned their backs on luxury in just two years. These are not occasional tourists forgoing a handbag in Paris while traveling; it is an entire segment of so-called “aspirational” customers that has evaporated, worn down, disappointed, or simply priced out by increasingly inaccessible costs.

Brands will need to rethink their luxury equations, restore creativity, and win back the trust of a clientele that feels betrayed.

The trap of price inflation

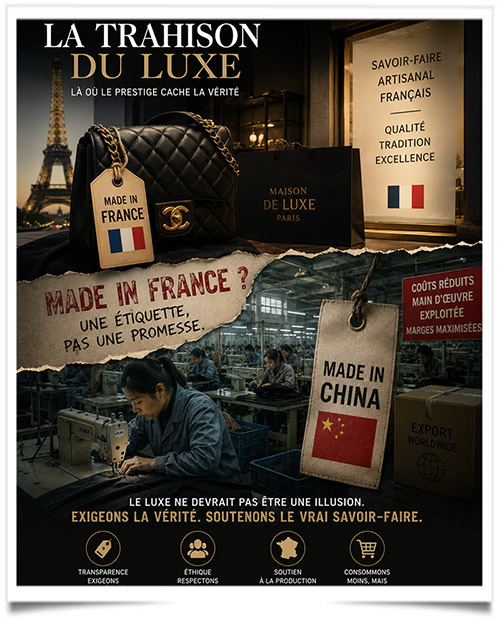

To understand this disengagement, one must look back at the aggressive pricing strategy adopted by major maisons starting in 2021. In a context of explosive post-Covid demand and global supply chain disruptions, brands used rising costs as a pretext to raise prices far beyond simple inflation pass-through. The result: an average increase of 21% between 2021 and 2023, with peaks reaching up to 45% on iconic items from Chanel or Louis Vuitton.

On the surface, the logic seemed flawless: in luxury, price is part of value. A bag that is too accessible loses prestige. Hermès has demonstrated this for decades with the Birkin. Scarcity and high pricing are the very promise of the product. But major maisons have confused exclusivity with greed.

Because simultaneously, and this is where the moral contract broke down, product quality did not keep pace. Consumers, especially Gen Z and millennials, compared, documented, and shared their disappointments on social media. Less refined linings, synthetic materials where leather once dominated, sloppy finishing on items costing thousands of euros. The relationship between perceived value and asking price visibly deteriorated, and digital word-of-mouth did the rest.

The silent erosion of quality

The issue of quality, long a taboo in luxury conglomerate boardrooms, was finally addressed at the Barcelona “Business of Luxury Summit.” Leading executives acknowledged, with varying degrees of candor, that the pursuit of volume and profitability had compromised the artisanal standards that underpin their maisons’ legitimacy.

LVMH recorded a 2% decline in revenue in the first quarter of 2025. Kering, owner of Gucci and Saint Laurent, saw its net profit collapse by 62% in 2024. These figures are not anecdotal; they signal a structural crisis of confidence, not a simple cyclical slowdown.

In this context, the second-hand market is booming. Vestiaire Collective saw its revenue grow by 20% over two years. Its co-founder Fanny Moizant stated it plainly at the Barcelona summit: in 2022, 50% of buyers on the platform cited affordability as their primary motivation. In 2025, that figure has risen to 78%. Second-hand no longer only attracts bargain hunters; it is now absorbing customers who, in the past, would have bought new.

The generational divide

Luxury brands long hoped Gen Z would become their natural successor clientele. The reality is more complex. This generation, born between 1996 and 2010, now represents around 10% of the luxury market and is expected to account for 40% by 2035. But its codes are radically different.

Before 2020

Young consumers aspired to traditional luxury codes: visible logos, iconic bags, branded clothing. Luxury consumption was a marker of social success.

2020–2022

The pandemic reshuffled priorities. Experiential luxury surged. Young wealthy consumers favored travel, wellness, and rare experiences over material goods.

2023–2025

Gen Z is turning away from new purchases in favor of second-hand, vintage, and cultural collaborations. 78% of users on resale platforms cite affordability as their main motivation.

This generation is not rejecting luxury; it is redefining it. According to Canal Luxe, luxury is no longer about what you own, but where you have been and what you stand for: hyper-personalized experiences, ethical commitment, authenticity. Affluent young consumers now spend on exclusive fitness classes, bespoke travel, and objects with verifiable stories. The cold display of logos no longer convinces them.

Paradoxically, brands have responded by doubling down on exclusivity, precisely the opposite of what this generation demands. By focusing on ultra-wealthy clients (VICs, Very Important Customers, who represent 2% of buyers but generate 40% of revenue), they have accelerated the loss of aspirational customers without guaranteeing the loyalty of the ultra-rich.

Luxury is undergoing one of its deepest transformations in decades. The overall stability of headline figures masks a profound structural shift.

The specter of inequality

Behind the luxury crisis lies a broader social reality: rising inequality is reshaping the market structurally. When middle classes see their purchasing power eroded by persistent inflation, discretionary spending, especially luxury purchases, is the first to be cut.

But inequality cuts both ways for the sector. On one hand, wealth concentration at the top fuels strong demand for ultra-luxury: yachts, exceptional properties, rare jewelry. The Middle East remains the most dynamic region in the sector. On the other hand, the erosion of affluent middle classes, historically the backbone of aspirational luxury demand, deprives brands of a crucial growth engine.

China, once the engine of global luxury, illustrates this tension. The 3–5% decline in Chinese demand in 2025 is not only due to economic slowdown; it also reflects an ideological shift. Part of the Chinese middle class is turning toward local brands, driven by a mix of national pride and resentment toward prices perceived as excessive among European maisons.

What should we take from this?

Luxury is not collapsing, but it is contracting and, above all, questioning itself. The loss of 50 million customers is not just a statistic: it signals a rupture in trust between major houses and a significant portion of their clientele.

For brands, the way forward requires deep work: restoring artisanal legitimacy, aligning prices with perceived value, and inventing new narratives capable of appealing to consumers whose values have profoundly evolved. This means accepting that 21st-century luxury will not be a repetition of the 20th. The crisis is real, but it carries within it the opportunity for reinvention. Luxury has always survived its crises, provided it understood why it created them.

FM